Time to end Help-To-Buy : The government’s state house builder subsidy.

It is a sad fact that homes remain unaffordable and it is difficult to get a mortgage unless you have managed to save a substantial deposit. “Help-To-Buy” the government’s “solution” is to subsidise the new home industry.

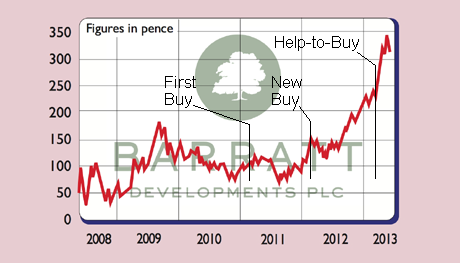

Since the first “state aid” for house builders ‘FirstBuy’ in March 2011, all the major house builders shares have soared, with many doubling in price and more! With the latest “incentive” ‘Help-To-Buy’ house builders do not even have to contribute anything, resulting in the biggest rise in their share prices since it became available in April 2013 (see the chart below.)

All three government schemes have helped house builders sell houses without having to reduce prices. This has resulted in a 50% plus increase in reported profits over the last year. As new home buyers now only have to find 80% of the price asked by house builders, many builders are actually increasing prices as the increased demand is not being matched by an increase in the number of new homes being built. Before the last property bubble burst in 2007, 200,000 new homes were built. The house builders currently estimate they will build just 110,000 this year, many on cheap land acquired during the last recession increasing profit margins even more.

Any increase in interest rates would cause a major problem for anyone buying these over priced state subsidised new homes, as a big fall in house prices is likely. Indeed this, together with the Help-To-Buy mortgage underwriting scheme has all the hallmarks of a government-sponsored house price bubble. There is a correlation between interest rates and house prices. As interest rates go up, prices fall and vice-versa. Keeping interest rates at artificially low levels can only further inflate house prices.

The Chancellor should impose a windfall tax on all house builders using Help-To-Buy on profits above 20% of turnover, with anything above being taxed at 80%. Failure to do so would leave many drawing the conclusion that costly government support for house builders and their wealthy shareholders, means we are most definitely not “all in it together” assuming we ever were!